Level 1 CFA® Exam:

Intro to Financial Reporting Quality

Welcome to the first lesson on financial reporting quality. In this lesson, we will discuss:

- financial reporting quality, earnings quality, and the relationships between these two,

- financial reporting quality assessment,

- accounting choices and departures from U.S. GAAP,

- aggressive vs conservative accounting.

We start by establishing the importance of financial reporting quality.

The quality of financial reporting is crucial both for analysts and investors.

As a rule, the financial reports that are prepared under the generally accepted accounting principles (GAAP) such as International Financial Reporting Standards (IFRS), Generally Accepted Accounting Principles in the US (U.S. GAAP), or any other home-country GAAP should demonstrate appropriate quality. That is because such generally accepted accounting standards provide the rules, guidelines, interpretations, and best practices to help companies with the preparation of clear, consistent, and comparable financial statements.

However, even GAAP-compliant reports may not always meet the analyst’s expectations. The analyst needs to be careful if the financial statements under scrutiny do not present an adequate level of reporting quality. Such financial statements may be misleading and they may fail to provide an accurate representation of the company’s performance and therefore make the analysis useless.

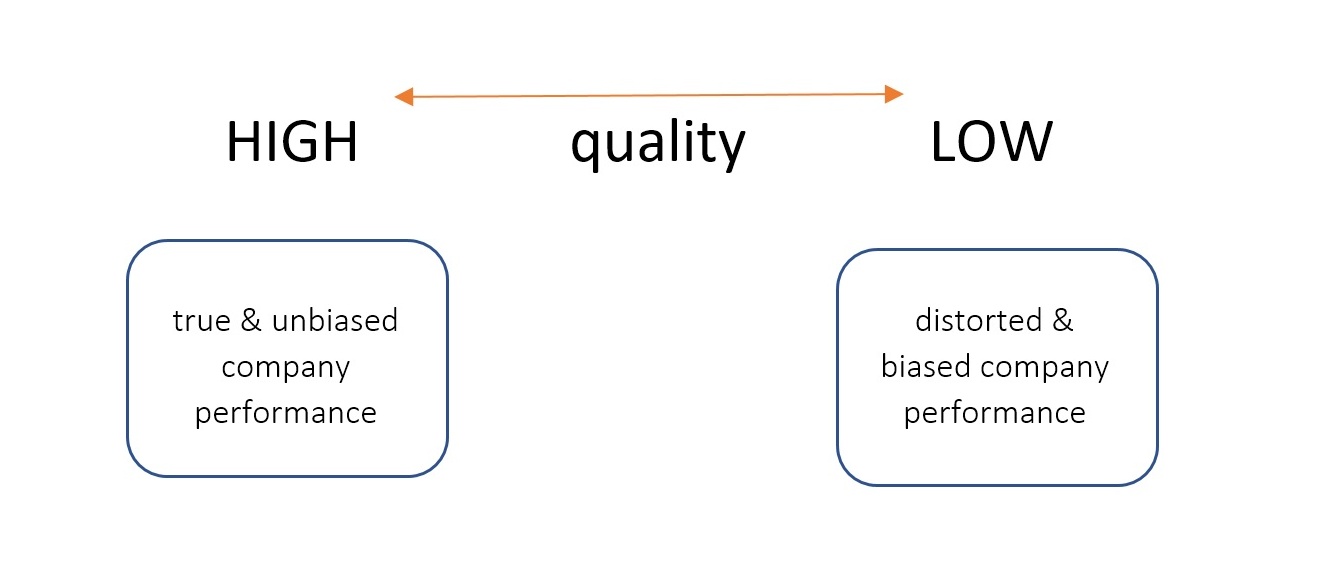

We distinguish between the reports that demonstrate high to low financial reporting quality.

At the higher end of the spectrum lie the financial statements that demonstrate a true and unbiased performance of the company, while the financial statements of the lowest quality are generally faulty and they might even intentionally distort the genuine condition of the company or include fictitious recording transactions.

Financial Reporting Quality Spectrum

Additionally, we also need to consider the earnings quality as a separate characteristic of the companies’ financial reports.

Earnings quality does not refer to the technical aspect of whether the business operations are faithfully and accurately reflected in the financial records (and therefore in the financial report).

Earnings quality refers to the sustainability of the revenues and cash generated by the company.

High-quality earnings provide a good return on the shareholder capital invested. It is worth noting that the high financial reporting quality is a prerequisite to high-quality earnings.

There is an observable positive correlation between the high quality of earnings and the valuation of the company. Analysts and markets are willing to promote companies that can generate results that are predictable in the future and based on a solid business model and market fundamentals.

Relationship between Financial Reporting Quality and Earnings Quality

star content check off when doneThe following table demonstrates the relationship between the high and low quality of financial reporting vs earnings quality:

| High Financial Reporting Quality | Low Financial Reporting Quality | |

| High Earnings Quality | Financial statements accurately reflect the performance and standing of the company, whose results are based on a robust business model. | Due to the low quality of financial reporting, analysts will not be able to appropriately assess whether the presented results are a true representation of the business performance. |

| Low Earnings Quality | While the financial statements accurately reflect company performance, the business model might not be sustainable and therefore negatively impact company valuation. |

An analyst needs to consider both financial reporting quality and earnings quality to understand where the company's financial reporting is on the spectrum of high (decision-useful) to low (not useful for analysis) quality.

(...)

We have already highlighted that the management may try to influence the way the data is presented in the financial statements. They do so by using biased choices within the limits of GAAP while still conforming to those accounting rules. However, such statements generally do not present the true performance of the company.

Aggressive vs Conservative

The management might be pressured to present a performance that is better than in reality and therefore it may apply accounting choices perceived as aggressive. Moreover, in certain circumstances, it might be beneficial for the management to present results that are worse than in reality by using conservative choices.

While aggressive choices are generally used to boost the company’s results in the current reporting period, conservative choices tend to be used when the management wants to decrease the results in the current period, so that it can increase the results in the future periods (i.e., by changing the bias from conservative to aggressive).

Aggressive accounting choices are used to improve company performance in the current reporting period (creates a sustainability issue).

Conservative accounting choices are used to inflate future results while decreasing company performance in the current reporting period (usually does not create a sustainability issue).

(...)

Companies may deliberately depart from the application of the GAAP standards. Such GAAP-incompliant financial statements should be perceived as of worse quality and usefulness in comparison with the ones that comply with GAAP (even if the management makes some biased choices or intentionally manages the results to the company’s benefit).

If the company’s financial statements fail to comply with the accepted standards, the analyst will struggle or will be completely unable to effectively assess the quality of the company’s earnings. So, the risk of not being able to properly value the company will be high.

EXAMPLE: In the past, there were multiple examples where firms such as WorldCom and Enron departed from GAAP to hide poor performance which eventually led to their bankruptcy.

Some companies not only depart from GAAP but also decide to intentionally mislead the market by producing fictitious or otherwise untrue reports (e.g., by recording transactions that never happened). Such financial reports are considered the worst on the quality spectrum and are of no use to analysts and market participants. Unfortunately, such cases are usually disclosed only after it is too late for investors to exit the investment.

As a rule, the distinction between conservative & aggressive accounting depends on judgment and interpretation of the users of financial statements.

Generally, biases and the application of the conservative or aggressive approach in accounting poses a challenge for analysts. The analyst needs to consider whether any adjustments to the financial statements under the analyst’s scrutiny are required to ensure the comparability and true representation of the company’s performance.

Importantly, while unbiased financial reporting is the most ideal one and it is widely promoted by the key GAAP (i.e., IFRS and U.S. GAAP), some of the commonly applied accounting principles are perceived as conservative.

EXAMPLE: While the revenues need to be almost certain to be recognized, some costs are allowed to be recognized when they are only probable.

EXAMPLE: While accounting standards between jurisdictions tend to be aligned, there may be some nuances that might indicate that the application of a particular standard will result in more conservative accounting treatment than if some other standards were applied (e.g., impairment of assets).

Some investors may be willing to accept the bias, especially if it is conservative. Such bias, while not presenting the most objective view of the company’s performance, might lead to positive surprises, which is good because investors will accept a surprise that is positive, e.g., analysts expected USD 100m net income but the company has reported USD 120m.

Let’s now have some typical examples of the conservatism within the accounting rules under both U.S. GAAP and IFRS:

- research costs, which are expensed as incurred (under U.S. GAAP), rather than capitalized (under IFRS, if certain criteria are met),

- litigation losses, even though they are still uncertain until the legal proceeding is finished, accounting standards require recognition when those become probable,

- insurance receivables, expected from the insurance company as a result of the insurance event, might not be fully recognized until the insurance company confirms the validity of the claim.

(...)

Biases: "Big Bath"

Worth noting here is a special case of companies that are undergoing restructuring. The judgmental nature of the restructuring charges estimation might encourage the management to recognize high losses during that period to build a "low basis". Then, in the following periods, the positive effects of the restructuring (as the future results are compared with the poor results from the restructuring period) might support the management’s “success story” and be perceived as a successful turnaround. Such behaviors are usually referred to as “big bath” restructuring charges or “cookie jar reserve accounting”.

Level 1 CFA Exam Takeaways for Intro to Financial Reporting Quality

star content check off when done- The quality of financial reporting is crucial for analysts and investors to be able to effectively assess company performance and value it for investment decision-making purposes.

- The assessment of the financial statements’ quality needs to focus on two things: whether the management applies accounting principles appropriately and if earnings quality is sufficient and sustainable.

- The reporting principles applied by the key governing bodies such as IASB or FASB provide a standard on how to produce high-quality financial reporting. Still, the management has a certain level of discretion over accounting choices, which means that no financial statements can be guaranteed to be “error-proof”.

- The management might consider aggressive accounting choices that improve performance in the current reporting period or conservative accounting choices that will inflate future results.

- Companies that decide to depart from GAAP, will generally be at risk of producing low-quality financial statements.

- Even GAAP might demonstrate certain elements of conservatism within their standards. Examples include research costs, litigation losses, and insurance receivables.

- Company acquisitions and restricting processes create a good opportunity for the management to manipulate financial performance.