Money-Weighted vs Time-Weighted Return CFA® Exam Cheat Sheet

When you put your money to work, sooner or later you simply want to know how successful the investment has turned out to be. To evaluate the investment merits, you need to measure the rate of return and assess the performance. The money-weighted rate of return measure and the time-weighted rate of return measure will come in handy then.

This blog post was created as a part of the CFA exam review series to help you in your level 1 exam revision, whether done regularly or shortly before your CFA exam.

Holding Period Return (HPR)

You must know that portfolio measurement is not as easy a concept as it may seem and especially in your level 1 CFA Exam it might turn out to be quite challenging or even problematic.

The basic concept connected with the return on an investment portfolio is the holding period return (HPR):

\(HPR=\frac{P_1+D_1}{P_0}-1\)

Where:

- \(HPR\) – holding period return

- \(P_1\) – price at the end of the period

- \(P_0\) – price at the beginning of the period

- \(D_1\) – dividend at the end of the period

So, HPR is the total return earned by an investor over a single period and it includes all cash flows occurring at the end of the period.

HPR is a valuable tool when you want to calculate the rate of return on an investment over one period assuming that no additions or withdrawals of money occur meanwhile. However, how should we compute the rate of return on the portfolio over many periods if there are cash inflows and outflows?

In such a case, we have two alternative measurement tools at our disposal, that is:

- the money-weighted rate of return, and

- the time-weighted rate of return.

Level 1 CFA Exam: Money-Weighted Rate of Return

The money-weighted rate of return is simply an internal rate of return (IRR). However, we use the term internal rate of return in the context of capital budgeting. In portfolio management, this measure is called the money-weighted rate of return. How was this term coined? Well, the money-weighted return accounts for the value of cash flows in given periods. So, logically the values of particular cash flows affect the value of the money-weighted rate of return.

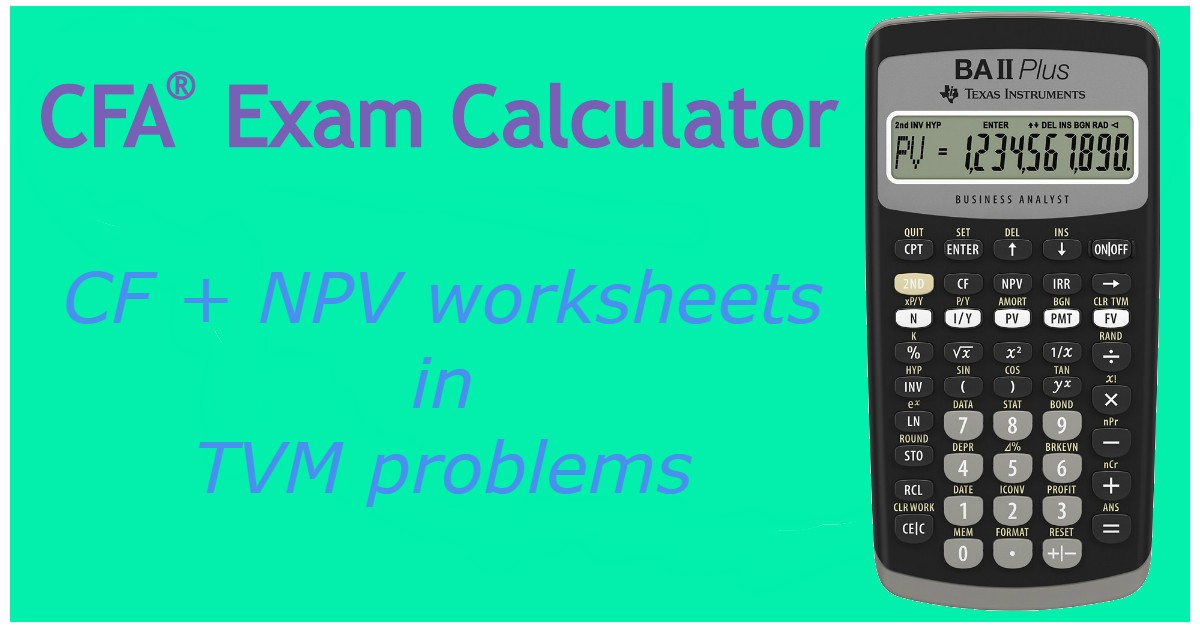

The money-weighted rate of return is calculated by equating discounted cash inflows to discounted cash outflows, but in the exam we’ll use Cash Flow and IRR worksheets.

An investor purchased 10 shares of a technology company for USD 50 each. After a year, he received a per-share dividend of USD 7 and sold 4 shares for USD 55 each. The investor decided not to reinvest the dividends. At the end of the second year, he sold the remaining 6 shares for USD 60 each. What is the money-weighted rate of return on this 2-year investment?

- 15.76%

- 16.31%

- 18.67%

Answer: C

We can compute this rate of return using a calculator. We're going to use the Cash Flow and IRR spreadsheets.

We open the Cash Flow worksheet and enter the following:

[2ND] [CE|C] (to clear the worksheet)

CF0=500 [+/-] [Enter] (there is a minus sign because we bought 10 shares for USD 50 each = it’s an outflow)

C01=290 [Enter] (because after one year we received a dividend in the amount of USD 7 for each of 10 shares and we sold 4 shares for USD 55 each)

C02=360 [Enter] (because at the end of the second year we sold 6 shares for USD 60 each)

Finally, we press the IRR button, press the CPT button, and get the result. The money-weighted rate of return is 18.67% annually.

Exam tip

You should develop a habit of clearing worksheets. Otherwise, previous data may mess up with your future computations.

Level 1 CFA Exam: Time-Weighted Rate of Return

The time-weighted rate of return differs from the money-weighted rate of return as it does not depend on the value of particular cash flows. The time-weighted rate of return is a geometric mean return over the whole investment period:

Where:

- \(TWRR\) – time-weighted rate return

- \(HPR\) – holding period return

An investor purchased 10 shares of a technological company for USD 50 each. After a year, he received a per-share dividend of USD 7 and sold 4 shares for USD 55 each. The investor decided not to reinvest the dividends. At the end of the second year, he sold the remaining 6 shares for USD 60 each. What is the time-weighted rate of return on this 2-year investment?

- ...

- ...

- ...

Example 2 is available for CFA Program candidates using our study planner to control their prep:

Already using Soleadea? 1. Sign into your account 2. Refresh this page to see Example 2.

Exam tip

When calculating the time-weighted rate of return you don't need to know the number of shares that were bought/sold (this data is redundant). You only need to know the prices of stock in different periods and the value of dividends.

As you can see the money-weighted rate is higher than the time-weighted rate of return. Is that a rule? Nope. Depending on numbers it could be the other way round.

Please also note that the time-weighted rate of return gives the same weights to different periods, whereas the money-weighted rate of return gives different weights to different periods. In this particular example with the money-weighted rate of return, a higher weight will be given to the first period as the beginning value in the first year was USD 500 and in the second year it was only USD 290. Since HPR for the first year is higher than for the second year and the money-weighted rate of return gives a higher weight to the first period, the money-weighted rate of return must be higher than the time-weighted rate of return.

Performance of Portfolios: Application

In the previous paragraph, we learned that the money-weighted rate of return gives different weights to different periods, while the time-weighted rate of return gives the same weights to different periods. Therefore, we should conclude that if an investment manager has full control of the timing of cash inflows and outflows, we should use the money-weighted rate of return. It would be appropriate in the case of our private investments when it is we who decide what amounts we invest in every period. When the portfolio manager has little influence on the invested amounts, we should apply the time-weighted rate of return. This is the case with a fund manager, who doesn’t have control over how much the clients add to or withdraw from the fund.

Level 1 CFA Exam Takeaways: MWRR vs TWRR

Here are things that you should remember/know about on your exam:

- The money-weighted rate of return is an internal rate of return (IRR).

- The time-weighted rate of return is a geometric mean return over the whole investment period.

- You should remember to clear calculator worksheets before doing any computations.

- To calculate the money-weighted return we use the CF and IRR worksheets (in your calculator remember to enter a minus sign in case of outflows).

- When calculating the time-weighted return instead of calculating HPRs for consecutive periods it would have been faster if we computed 1 plus HPRs for these periods.

- When calculating the time-weighted rate of return you don't need to know the number of shares that were bought/sold. You only need to know the prices of stock in different periods and the value of dividends.

- Generally, the money-weighted and the time-weighted returns are not equal. Exception: If throughout the investment period, the investor does not sell any shares, nor does he purchase any new ones, and all received dividends are reinvested, then the money-weighted rate of return is equal to the time-weighted rate of return.

- An investment manager has full control of the timing of cash flows use money-weighted return for the manager's evaluation; otherwise time-weighted return is preferable.

For better knowledge retention: download, print, and add your own notes >>>

LAST UPDATE: 2 Nov 2023

Read Also: