Level 1 CFA® Exam: 4 Methods of Bond Valuation

This blog post was created as a part of the CFA exam review series to help you in your level 1 exam revision, whether done regularly or shortly before your CFA exam.

Bond Valuation: Price of a Well-Priced Bond

The price of a well-priced bond is equal to the present value of the future cash flows from the bond, namely coupons, and the bond’s par value. So, to value a bond we need to know the discount rate used to discount the cash flows.

The value of the discount rate depends on the risk associated with the bond’s cash flows. Therefore, if we have two bonds with different credit ratings, we should apply the higher discount rate when valuing the bond with the lower rating, that is the more risky bond, and the lower discount rate when valuing the less risky one.

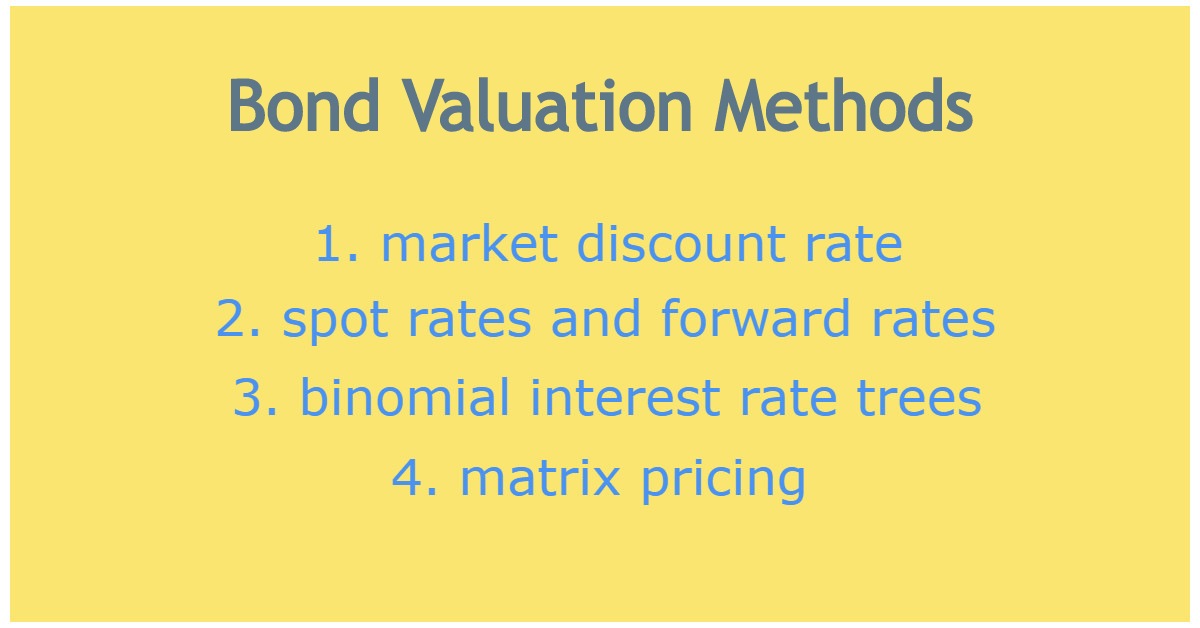

4 Methods of Bond Valuation

Generally, we have four methods of bond valuation at our disposal. Each is based on the time value of money concept. What distinguishes these methods is the applied discount rate. We can value a bond using:

- a market discount rate,

- spot rates and forward rates,

- binomial interest rate trees, or

- matrix pricing.

Bond Valuation Using Market Discount Rate

The first method is the simplest one. It assumes using only one discount rate (aka. discount market yield, required yield, market discount rate, required rate of return) for the entire period from today to the maturity date.

To find the bond value today, we use the following formula:

\(V_0=\frac{C}{1+r}+\frac{C}{(1+r)^2}+…+\frac{C}{(1+r)^{n-1}}+\frac{C+FV}{(1+r)^n}\)

Where:

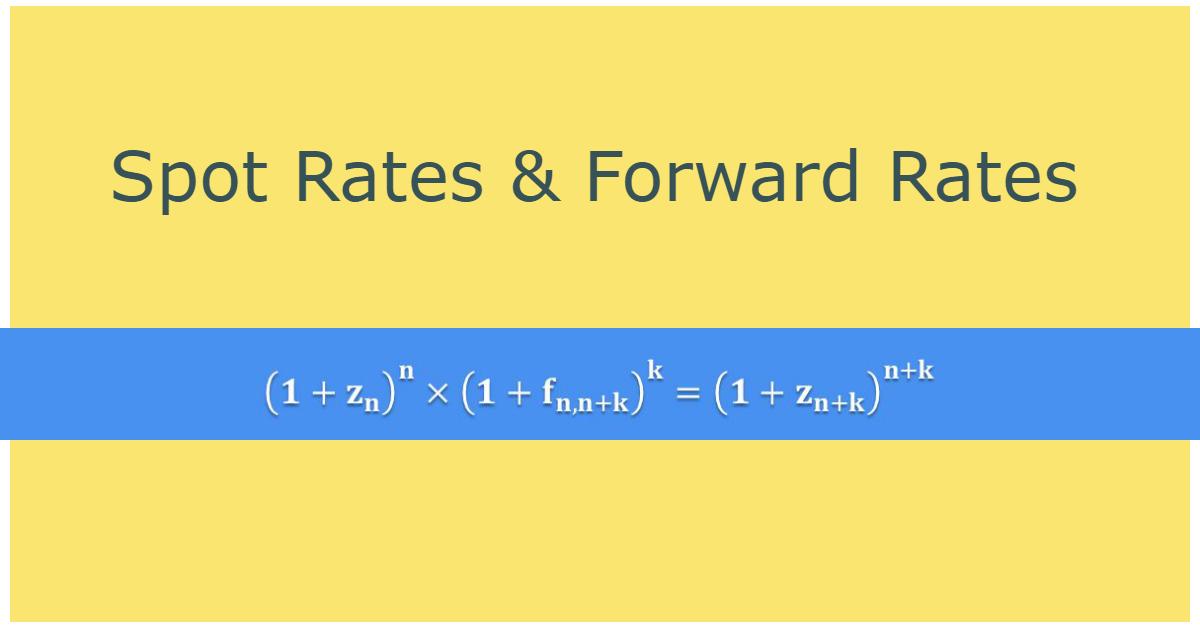

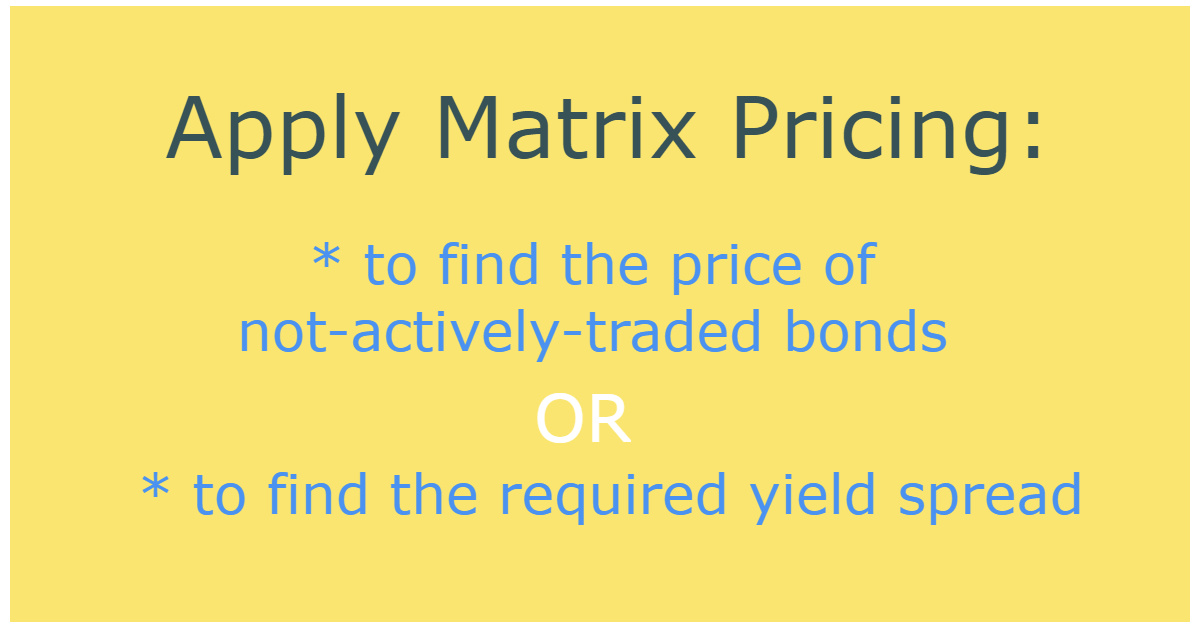

\(V_0\) – bond’s value today, C – bond’s coupon, r – market discount rate, n – time until maturity, FV – bond’s par value. If you need to refresh your knowledge about bond features before your level 1 CFA exam, read this study lesson An investor wants to value a six-year Bond X with a par value equal to USD 100 that pays coupons annually. The coupon rate equals 5%. Assuming that the market discount rate is equal to 6%, Bond X value is closest to: Answer: A Let's use the BOND worksheet to compute the bond's value: Press [2ND] [9] to access the BOND worksheet SDT = 1.0100 [Enter] (we set the start date to 1 January 2000) CPN = 5 [Enter] (coupon is equal to 5%) RDT = 1.0106 [Enter] (because the bond matures in 6 years we set the redemption date to 1 January 2006) RV = 100 [Enter] (because the redemption value is equal to the par value; if the value is already 100 don't press [Enter], only ) frequency of coupon payments: 1/Y - once a year ; if you have 2/Y on the screen, press [2ND] [Enter] to set it to 1/Y YLD = 6 [Enter] PRI = [CPT] = 95.0827 The bond price is USD 95.0827 per USD 100 of par value. An investor bought a six-year Bond Y with a par value equal to USD 100 that pays coupons annually. The coupon rate equals 5%. Assuming that the bond value is USD 103, the market discount rate is closest to: Question 2 is available for CFA exam candidates using our study planner to control their prep: Already using Soleadea? 1. Sign into your account 2. Refresh this page to see Question 2. The second method of bond valuation assumes the use of a set of spot rates (or alternatively forward rates) to discount the cash flows from the bond. We can say that the spot rate is the interest rate applicable to the period from today to some point in time in the future, and the forward rate is the interest rate applicable to two periods in the future. Spot rates for different periods usually differ from each other. For example, the value of a spot rate for the period from today to the end of the first year is usually different than for example the value of the spot rate for the period from today to the end of the second year. The same holds for forward rates. For example, the forward rate for the period from the third to the fourth year will be different than the forward rate for the period from the fifth to the sixth year. In the case of bond valuation based on spot rates, each of the bond’s cash flows will be discounted by a different spot rate applicable to the given cash flow. Similarly, we use a whole set of forward rates (instead of one discount rate) to discount bond cash flows when we want to use forward rates to value bonds. For comparison, in the case of the bond valuation method based on a market discount rate, we use the same discount rate for every cash flow as explained above. You can learn more about spot rates and forward rates and how we can use the rates to value bonds in this blog post The bond valuation method that applies binomial interest rate trees assumes that interest rates are volatile. As a result, in a given period the discount rate can take different values. The further the period we consider, the more different values of the interest rate we have at our disposal. We use interest rate trees to value bonds with embedded options. This is because in this method we can take into account the fact that the bond may be sold by the bondholder or bought back by the issuer before the maturity date. As we already know, exercising the call or put option changes the cash flows of the bond, and this change can be taken into consideration in this method of bond valuation. In the case of the first two methods, we can’t take changes in the bond’s cash flows easily into account. Binomial interest rate trees are suitable for valuing not only the bond itself but also the embedded option. The valuation using interest rate trees is not tested in the level 1 CFA exam. The fourth method of valuing bonds, namely matrix pricing, is a variation of the first method. In the first method, we assumed that the discount rate is known. Under the matrix pricing method, it is assumed that we do not know the discount rate at the beginning. We use matrix pricing to determine it. To compute the discount rate, we use the linear interpolation and yields to maturity of similar bonds, where similar means – for example – with similar risk but different maturity dates. We will use matrix pricing either when the bond valued is illiquid or when we intend to value the bond that is to be issued in the near future. We discuss matrix pricing in a separate blog post here LAST UPDATE: 2 Nov 2023 Read Also:

Bond Valuation Using Spot Rates & Forward Rates

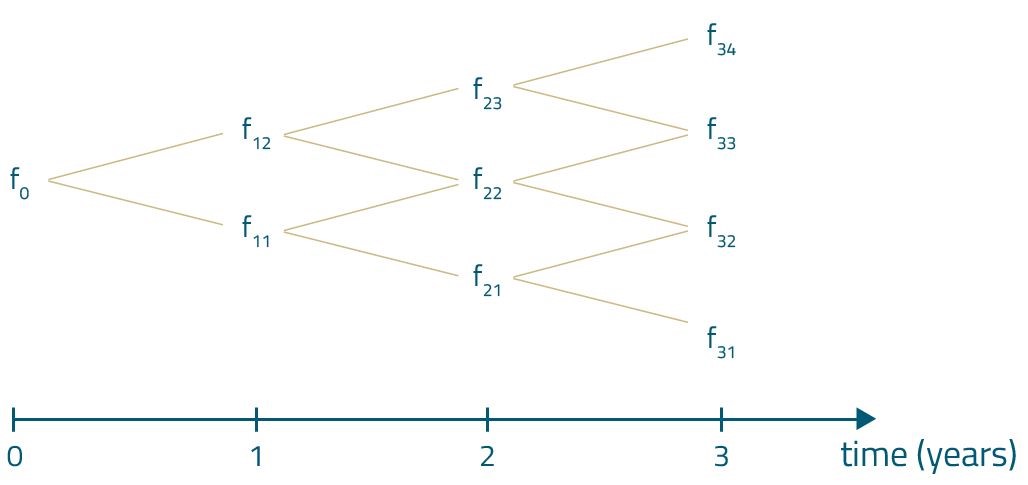

Bond Valuation Using Binomial Interest Tree

Bond Valuation Using Matrix Pricing

Level 1 CFA Exam Takeaways for Bond Valuation